Another banking crisis – How are REITs positioned?

To download a PDF version of this update, click here.

Executive Summary

The recent failure of several regional US banks and Credit Suisse has triggered concerns about the impacts for commercial real estate (CRE) markets as, to varying degrees, these financial institutions are an important source of finance.

- Banks account for around half of total CRE mortgage debt outstanding in the US.

- The top 25 banks account for approximately 15% of total CRE mortgage debt outstanding, and those loans represent only 5% of the assets of these banks.

- Smaller banks (of which there are over 4,600 in the US) account for around 38% of total CRE mortgage debt outstanding and represent a more meaningful 25% of the assets of these banks.1

- Excluding lending to owner occupied properties and farmland, loans from small banks account for around 8% of the total estimated value of income-producing CRE in the US.

After a period of easy money and historically low real estate loan defaults, we do expect heightened credit losses as the market returns to more moderate monetary and fiscal policy settings impacting tenants, landlords and financiers. This should be viewed as a return to ‘normal’.

Crucially at this point, we see limited signs of excess specific to the commercial real estate sector which would cause systemic failure. Furthermore, in general, the listed REIT sector appears to be at least relatively well positioned.

However, there are reasons for vigilance. Clearly, for a variety of reasons, the US office market is an outlier as it faces something of a crisis which could trigger broader ramifications. Moreover, there is limited visibility on the private lending market where higher leverage could cause distress and capital flight.

This report seeks to provide context around:

- the magnitude of these issues for U.S. commercial real estate generally

- the state of the REIT market with a particular focus on the situation in the U.S.; and

- a focus on US office, the sector most at risk

Overall, whilst it will be far from easy, we find that there are important differences between the current malaise compared to the credit crunch that led the Global Financial Crisis. Furthermore, listed REITs are well placed to capitalise on any distress that may arise in the broader real estate investment market.

Commercial property and the new banking crisis

Recent changes to monetary policy and consequent pressures on the economy and banking system has cast the spotlight on the state of lending to the commercial property sector. All eyes are now on the liquidity of key parts of the banking and finance sector, the status of non-performing loans, related and unrelated to commercial real estate, as well as the risk of deposit flight.

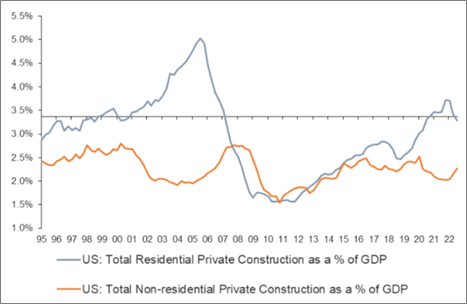

Naturally comparisons are being made between the current situation and the Global Financial Crisis some 15 years ago. We believe there are key differences. As illustrated in the following chart, the past decade of quantitative easing and low interest rates has not translated into excessive construction lending for new commercial building development – which stands in stark contrast to the boom in residential construction in the lead up to the GFC.

US residential and non-residential construction as % of GDP

Source: Bloomberg, US Census Bureau

Importantly, thus far, the banking failures do not appear to have been caused by problems in commercial property exposures. Rather they relate largely to lending practices to other parts of the economy (e.g., tech start-ups and crypto) and to poor bank capital management associated with asset-liability matching and depositor concentration.

Although arguably still early in the current crisis, with few exceptions, we believe the credit quality of the income producing commercial real estate sector today is better than the sub-prime borrowers of the early-mid 2000’s.

Nevertheless, currently at historically low levels, we expect there will be rising commercial property loan defaults thereby exacerbating issues in the banking sector. We believe these emerging issues are likely to emanate from loans to highly levered landlords and those property sub-sectors experiencing challenging operating conditions such as the US office market. Crucially, as we explore in more detail in a later section of this report, listed REITs are generally well positioned and office property is a relatively small part of the Global REIT universe.

It is important, however, not to be complacent and recognise REITs do not operate in a vacuum. With smaller banks potentially sidelined, the CRE sector should encounter a period of tighter lending conditions as all borrowers are forced to pursue fewer active finance providers, themselves likely facing further regulatory lending controls. Furthermore, there is limited visibility on the magnitude of private/mezzanine lending to commercial real estate where higher leverage is commonplace. We note however that this channel is regarded as less systemically risky than the traditional banking sector – albeit its potential withdrawal would not be without broader consequences. Moreover, a deep and prolonged economic recession would also impact the operating fundamentals of real estate markets.

It is also worth considering medium to long term benefits from a moderate tightening of lending standards and higher return hurdles. A period of risk aversion should lead to less funding for new property development, ultimately leading to less competitive new supply added to the market which should benefit existing landlords that have resilient rental income streams, significant debt covenant headroom and limited need for additional capital.

Many REITs, and we believe particularly our portfolio, fit this profile enabling them to exploit the distress of those less well capitalised.

US commercial real estate capital market landscape

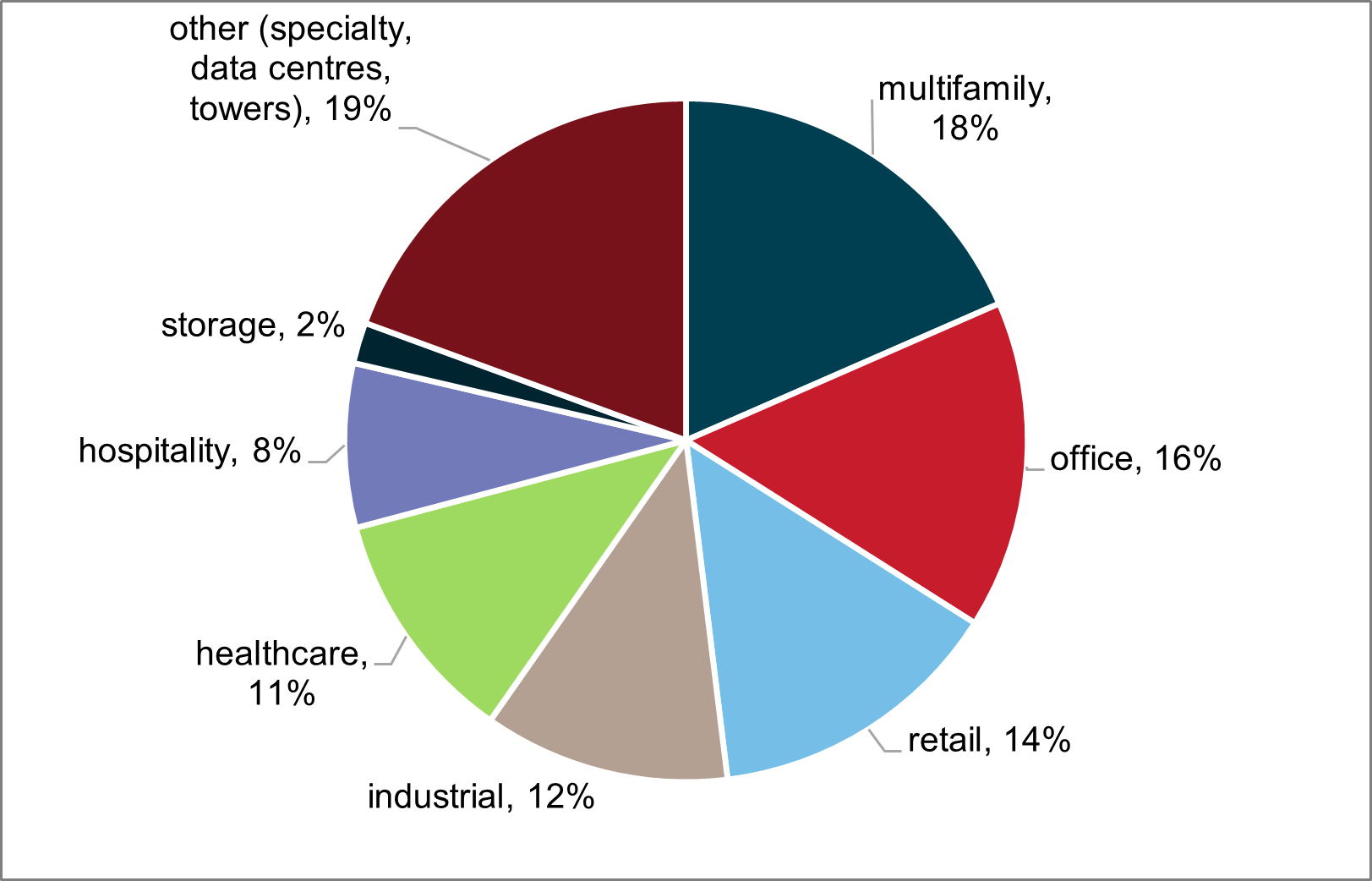

According to the National Association of Real Estate Investment Trusts (NAREIT), the total value of the US commercial real estate market was estimated to be approximately US$20 trillion2, of which US REITs represent around US$1.7 trillion.

US Commercial Real Estate Market total value by sector

Source: NAREIT, Co Star, June 2021

Total commercial real estate mortgage debt amounts to approximately US$5.5 trillion3. In addition, there is approximately US$700 billion of unsecured real estate debt issuance4. The size of additional sources of private market and mezzanine debt is less transparent, although Preqin estimates the size of the global private debt market (all sectors, not just real estate) at approximately US$1.2 trillion at the end of 20215.

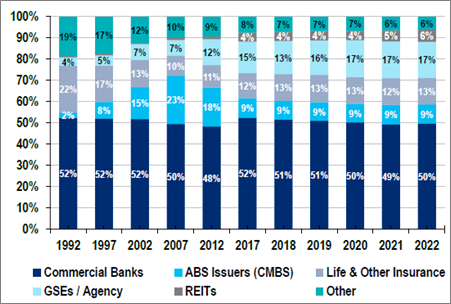

Of the US$5.5 trillion total mortgage debt, approximately 50% has consistently been provided by commercial banks since the early 1990’s.

Composition of commercial mortgage debt outstanding %

Source: Citi Research and Federal Reserve

Other major sources of mortgage debt include government agencies such as Fannie and Freddie (principally to the residential sector), life insurance companies, and the Commercial Mortgage-Backed Securities (CMBS) market.

The relevance of smaller banks

With recent US bank failures having principally been small / regional banks, attention has naturally turned to how important these banks are to the commercial real estate market. The Mortgage Bankers Association (MBA) defines smaller banks as those outside of the top 25 largest banks by total assets. Per MBA’s analysis, smaller banks (of which there are 4,690 in the US) account for around US$2.1 trillion of all CRE loans, or around 38% of total mortgage debt outstanding.6

‘Small’ banks therefore comprise a meaningful component of commercial mortgage lending in the US. Excluding lending to owner occupied properties and farmland, small banks account for around US$1.6 trillion of debt on income-producing commercial real estate – or 8% of the US$20 trillion estimated size of the CRE market.

Discussions with industry experts suggest small banks have a higher proportion of their assets (circa 25%) exposed to commercial real estate compared to larger banks and these loans are skewed to secondary and tertiary markets. The larger banks have approximately 15% of their assets in commercial real estate loans and are more focused on arguably higher quality and more liquid major cities and coastal markets.

Importantly, we note that smaller/regional banks are immaterial lenders to listed US REITs, with only a small number of US REITs sourcing less than 10% of their debt from such lenders. Credit Suisse is also not a prominent lender to listed REITs, while Deutsche Bank has been active in the broader property sector but not as meaningfully involved with REITs.

However insignificant the currently troubled banks are to the REIT sector, we acknowledge that distress within the banking sector will undoubtedly result in further tightening of lending conditions which will have a dampening effect on the broader commercial real estate market, particularly those sub-sectors facing operational challenges and high capital expenditure requirements such as the office sector.

Lending conditions

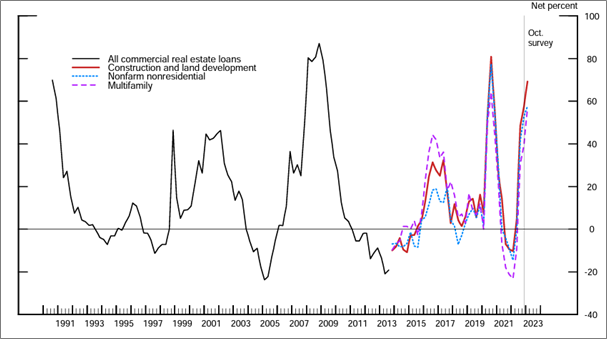

It is notable that even before news of the recent bank failures, the US Fed survey of senior loan officers in January 2023 was already indicating tighter lending conditions and weaker demand for all commercial real estate categories. As the following chart demonstrates, the survey readings were approaching peak levels seen in the GFC and Covid-19 pandemic. The key question will be how much further tightening occurs from here and for how long.

Net percent of domestic respondents tightening standards for commercial real estate loans

Source: Federal Reserve Board, Senior Loan Officer Opinion Survey on Bank Lending Practices January 2023

Note: For data starting in 2013:Q4, changes in demand for construction and land development, nonfarm non-residential, and multifamily loans are reported separately.

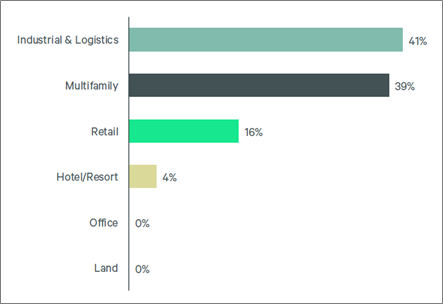

Meanwhile, a December 2022 survey of lending intentions by real estate broker CBRE indicated that lenders were still willing to lend to property sub-sectors with solid operating fundamentals such as logistics and multifamily, while risker areas such as development land, office, and hotels were least preferred.

Top 3 preferred property types for lending in 2023

Source: CBRE lending intentions survey Dec 2022

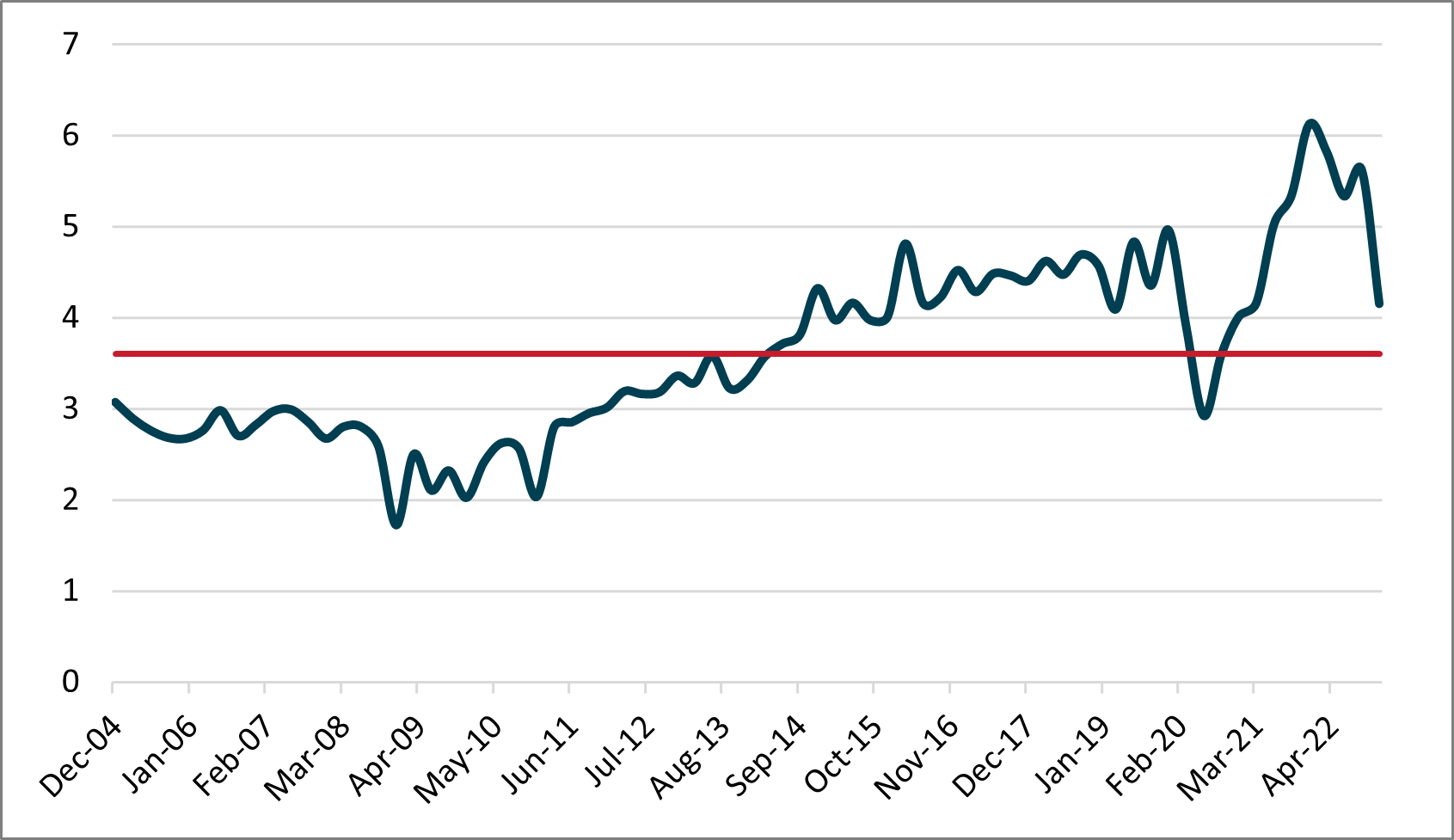

Delinquency rates

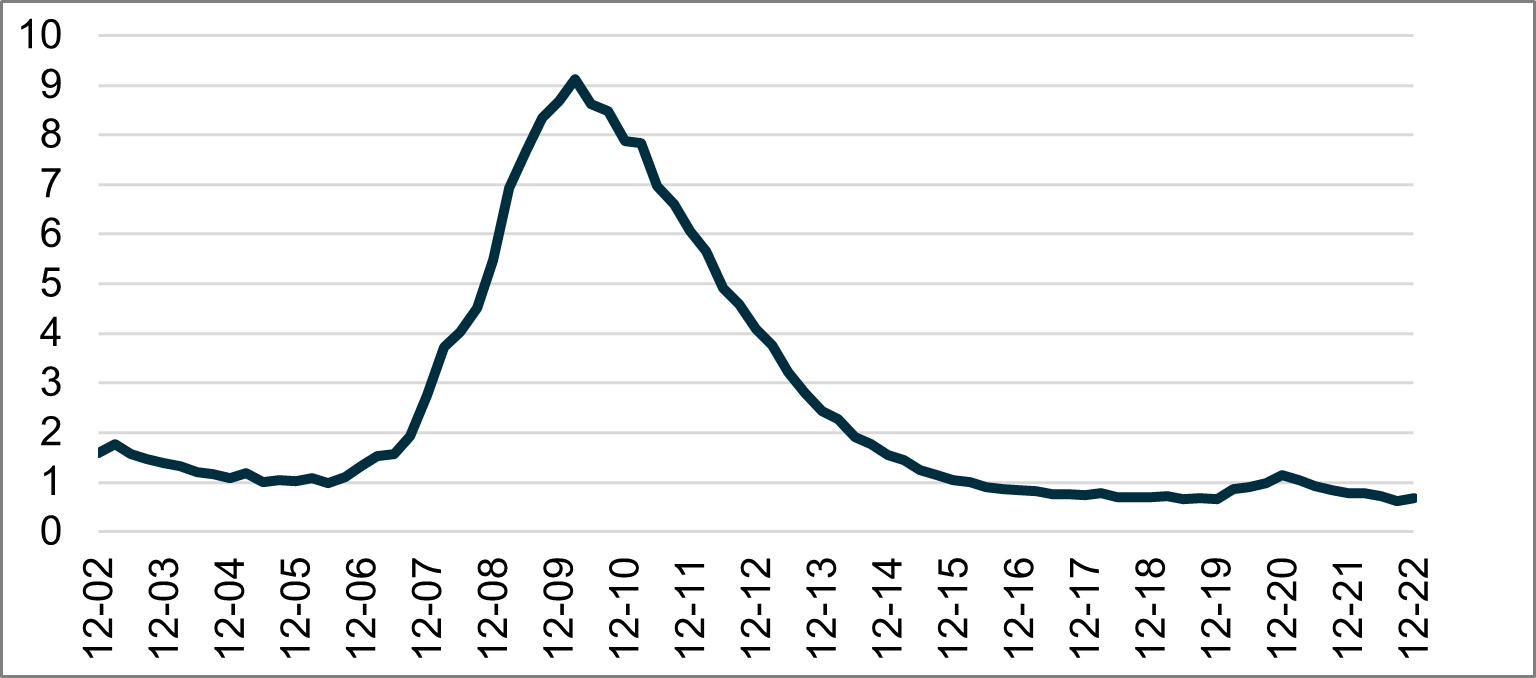

While there have been increasing reports of high-profile office landlords defaulting on CMBS loans, thus far bank loan delinquency rates remain low at under 1%. At the peak of distressed environments in the past, such as the GFC, delinquency rates spiked to 9%.

Delinquency Rate on Bank Loans to Commercial Real Estate

Source: Bloomberg, US Federal Reserve

Loans defaults that have been reported to date are predominantly in the CMBS market which often have lower quality assets and higher loan-to-value ratios. Some of the recent defaults have reportedly been used as a negotiating tactic by borrowers to extract better terms, thus described as ‘strategic defaults’. For example, some borrowers want to avoid the requirement to purchase expensive interest rate caps on floating rate loans which are automatically triggered when extension options are exercised.

Nevertheless, CMBS delinquency rates are also relatively moderate thus far with circa 4% of loans delinquent for 30 days and over. However, spreads on BBB-rated CMBS have risen, which makes it more difficult for banks to free up lending capacity by securitising existing loans.

While on the topic of loan defaults, it is worth touching on the historic case of US mall company General Growth Properties (no longer listed) which became the largest ever property bankruptcy in 2009. The GGP bankruptcy was largely attributable to its strategy of higher leverage and shorter maturities funded predominantly via the CMBS market. Particularly in the 5-year period prior to the GFC, the company had undertaken a huge acquisition spree which was predominantly debt funded. By 2007 its debt/EBITDA was 13.8x and its weighted average debt maturity was 4 years. Such leverage metrics are no longer common in the US REIT industry, as we illustrate in later in this report, with average net debt/EBITDA of 6.2x and >6.5yrs weighted average maturity.

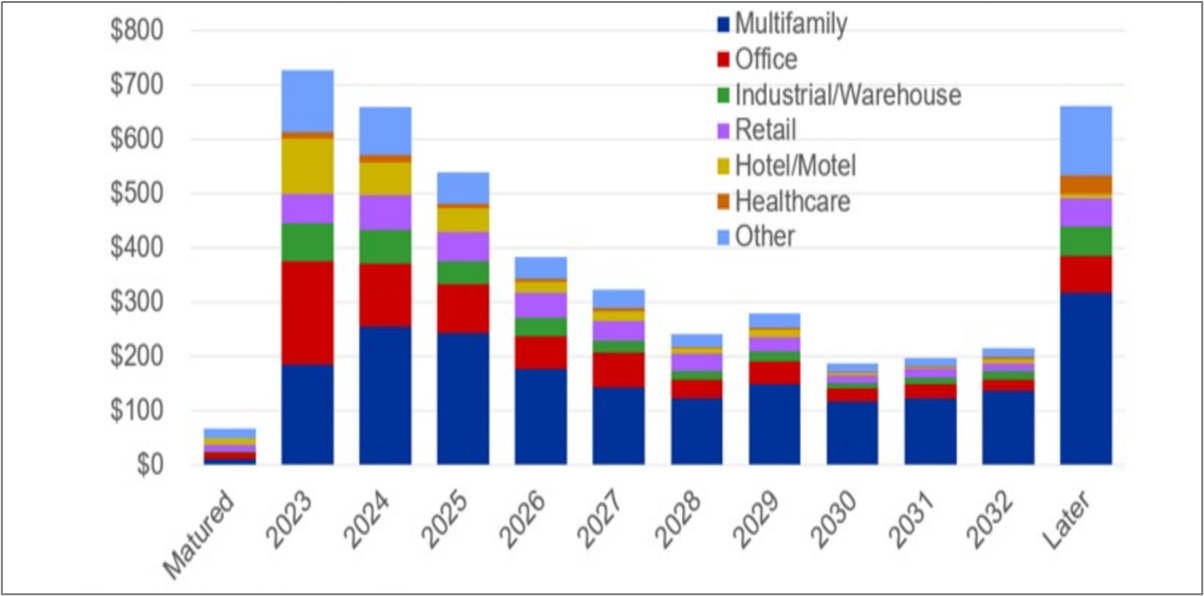

CRE Mortgage Loan Maturities

Approximately US$700 billion of mortgages (13% of total) are estimated to mature in 2023, with office being the largest sector expiring this year. Importantly, listed US REITs do not face the same risk profile as REITs have less than 5% of debt maturing in 2023.

Estimated total commercial mortgage maturities US$ billion

Source: Mortgage Bankers Association

Could US office be the breaking point?

Within the property industry, the US office market is experiencing the most challenging operating conditions as high and rising vacancy rates are expected to result in significant downward pressure on rental income and valuations. Hence, combined with rising finance costs, there is a strong possibility of a significant number of loan covenant breaches and outright defaults. Indeed, we have already seen high profile cases of landlords defaulting on loans and “handing back the keys”, including properties owned by vehicles associated with the likes of Brookfield, Blackstone and PIMCO.

US CBD office market vacancy rate

Source: Cushman & Wakefield

Listed US office REITs have not been spared, with share prices down between 50-75% from pre-pandemic levels – approaching similar peak-to-tough drawdowns experienced during the GFC. Evidence of the mounting stress, it hasn’t helped that three US office REITs (two of which have above-industry average leverage) have cut their dividends to preserve capital.

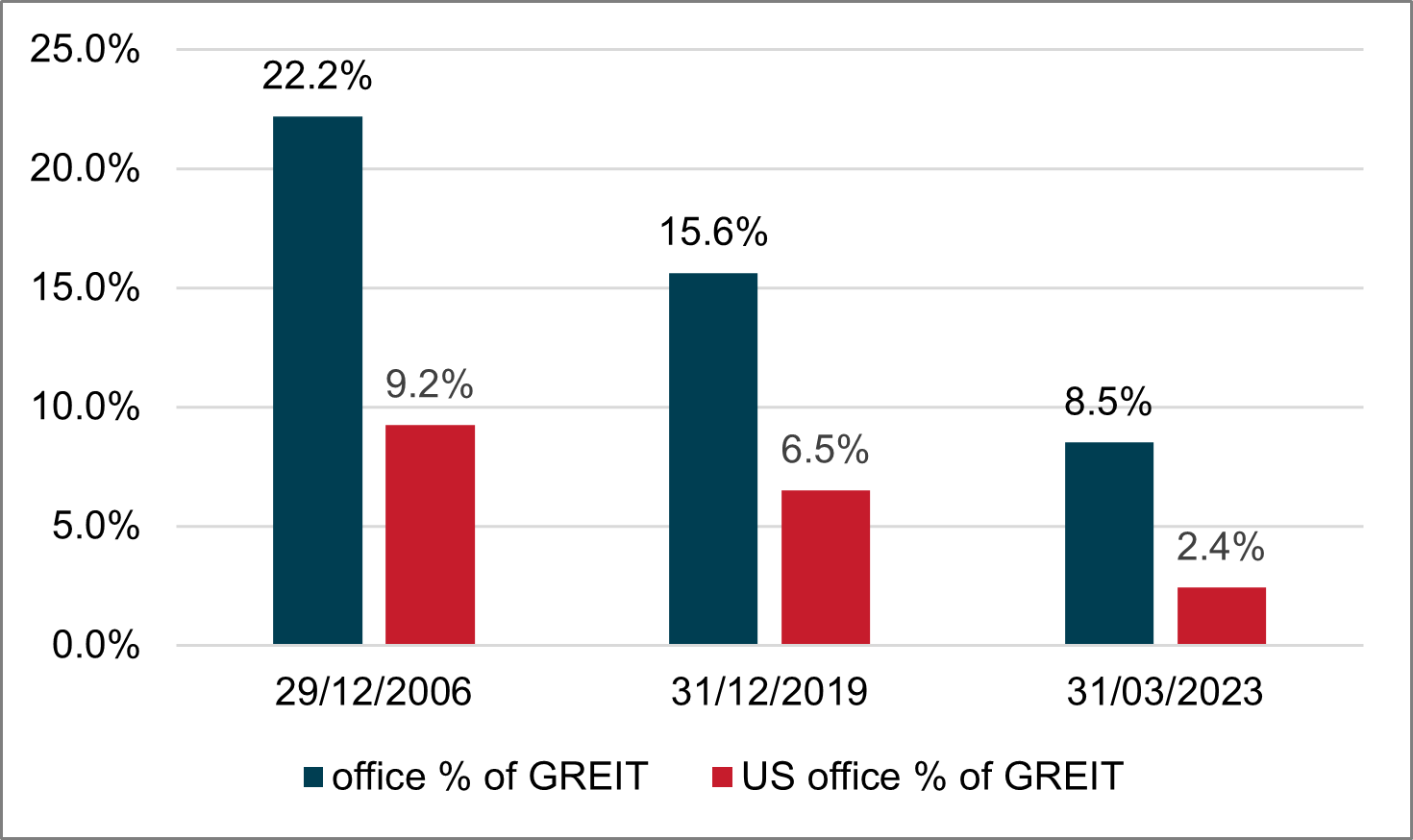

Notably, in the listed REIT sector at least, the trend away from office investment has been happening for some time with the global office property sector now representing just 8.5% of the Global REIT benchmark7 and the US office sector just 2.4%.

Office REITs as % of Global REIT Index

Source: Factset, Resolution Capital. FTSE EPRA NAREIT Developed Index. Note office sector excludes Life Science specialists Alexandria (ARE) and Biomed (BMR).

The Resolution Capital global REIT portfolio has had an underweight exposure to the office sector since early 2020 and currently has ~1% exposure to traditional US office and a further ~1% to all forms of specialist office REITs (excl medical office buildings).

Nevertheless, whilst office is a relatively small segment of the REIT sector, many pension funds and private real estate investors are not as well positioned. Hence, the parlous state of the overall US office property market is of particular interest as it potentially threatens bank lending capacity for real estate more broadly.

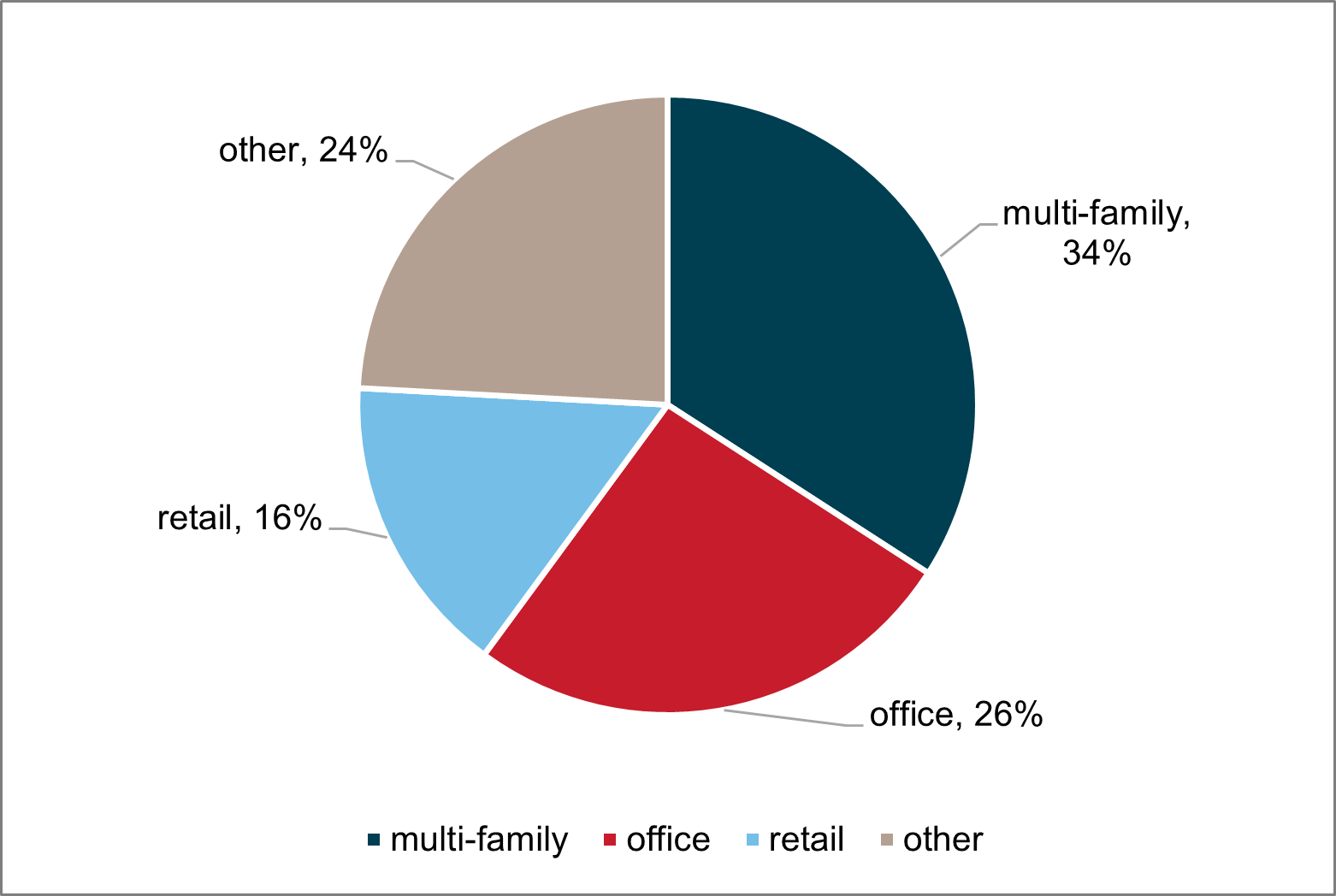

It is estimated that approximately 26% of loans provided by commercial banks is secured against office properties.

Bank debt property sector composition

Source: JP Morgan, Mortgage Bankers Association 2023 – proportion of commercial and multi-family loans

US REIT debt analysis

Significantly, while there are a few rare exceptions, US REITs have a much stronger leverage profile than the average commercial real estate investor. Of the 88 US REITs with an S&P credit rating, 75% have the scale and strength to warrant an investment grade rating. This opens more avenues to access debt finance, with longer duration, less onerous covenants and typically lower interest rates.

At least partly due to their credit ratings, critically, US REITs are not reliant on banks (large or small) for finance as they source of most of their debt from the unsecured bond market. Hence, the greater direct risk for US REITs would be a dysfunctional corporate bond market, which is not currently evident.

Other sources of debt for REITs include life insurance companies, a relatively small exposure to Commercial Mortgage Backed Securities (CMBS) and banks, the later often used as a provider of Lines of Credit which are typically used as working capital facilities.

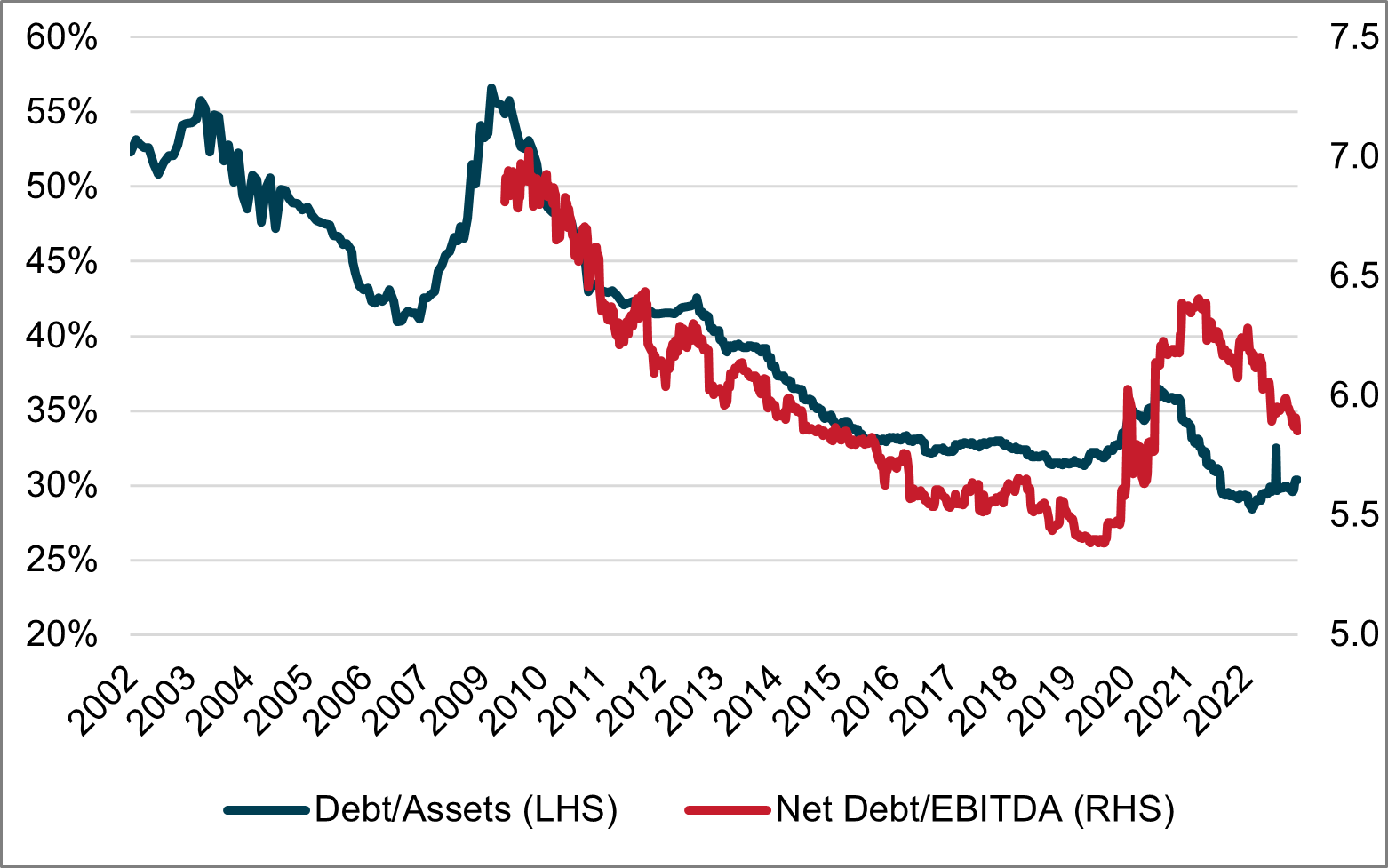

We expect minimal loan defaults by US REITs due to several factors. As the following charts show, US REITs have:

- Modest financial leverage – typically in the range of 6x net debt/EBITDA or circa 30% debt to assets, well below lending covenants. This compares to non-REIT CMBS where leverage is typically above 50% debt/assets and private equity funds where leverage can be much higher.

US REIT Debt / Asset Value and Net Debt/EBITDA

Source: Green Street Research

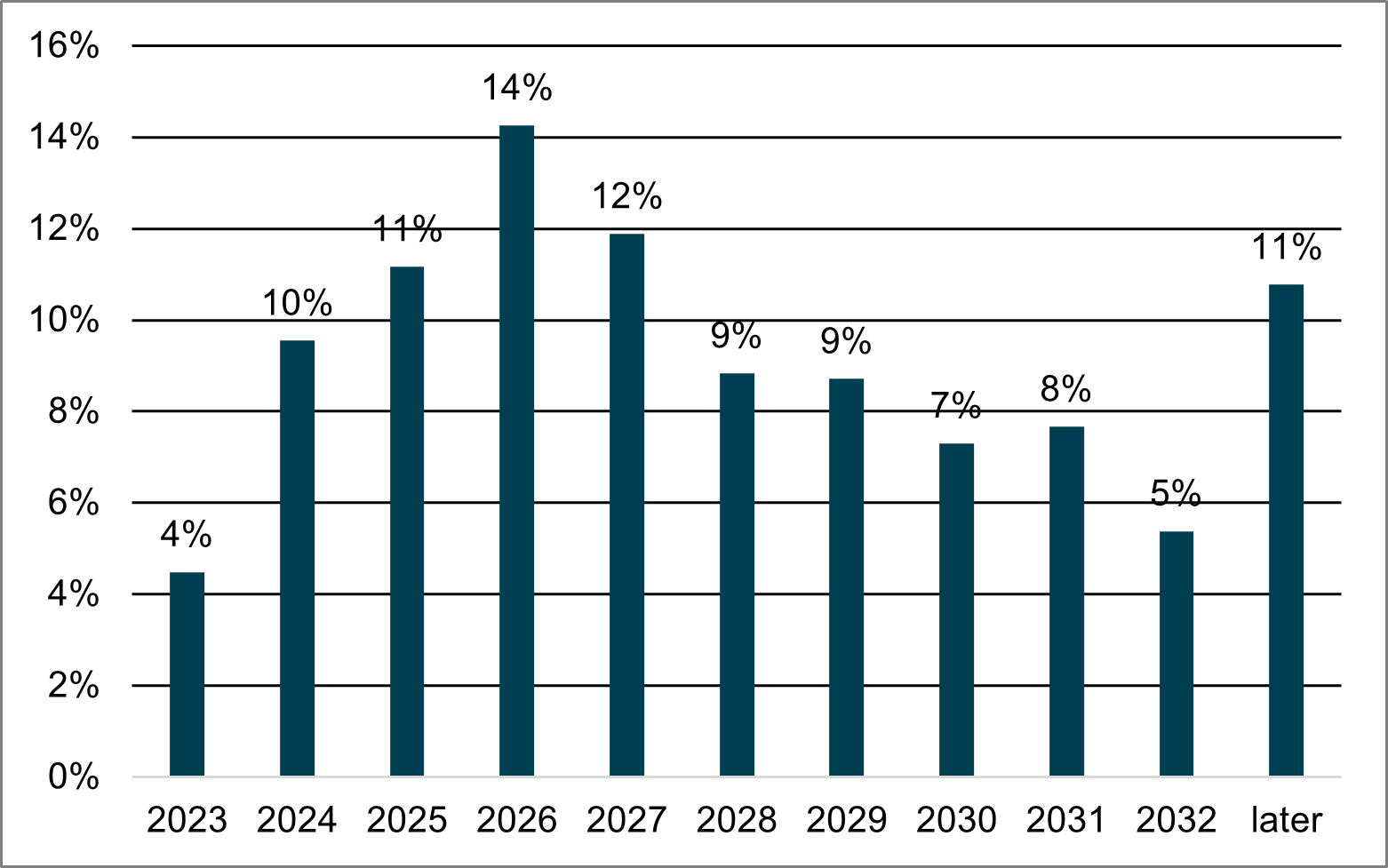

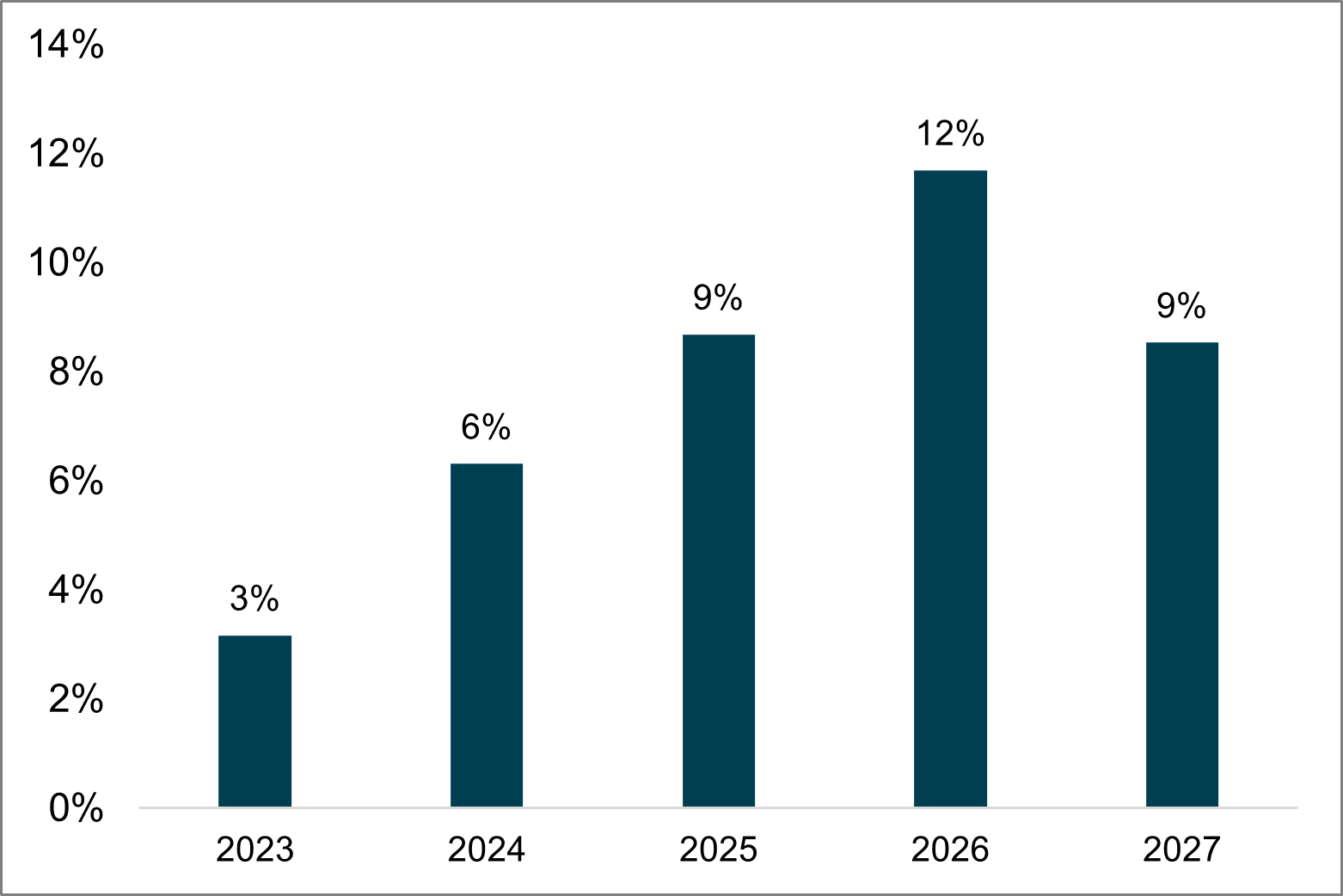

- Limited near-term debt maturities – with only 4% expiring in 2023 and a further 10% in 2024.

US REIT debt maturities – low in the near term

Source: Factset, Citi Research

- REITs have an average remaining debt maturity of over 6.5 years, the majority of which is at fixed interest rates. Hence the REITs have limited refinance risk and low likelihood of breaching ICR covenants.

US REIT average debt duration – increased since the GFC

Source: Bloomberg, NAREIT

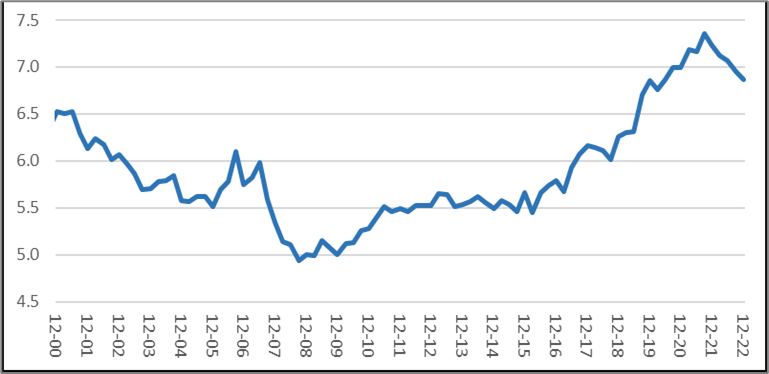

- Healthy debt service coverage, with interest coverage ratios averaging 4x, compared to the long-term average of 3.6x

US REIT interest coverage ratio – above long term average

Source: S&P North America REIT, Capital IQ

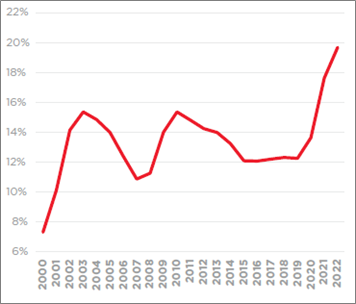

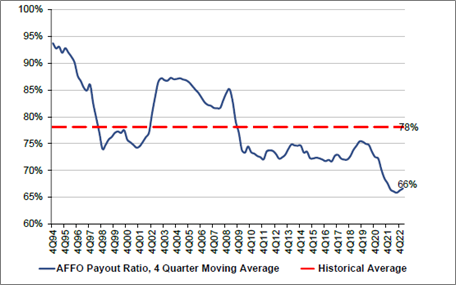

- Conservative dividend payout ratios (66% of Adjusted FFO, the lowest rate on record) which means REITs are retaining earnings to fund ongoing capex to maintain competitiveness.

Historical U.S. REIT Dividend Payout Ratios – lowest on record

Source: Citi Research

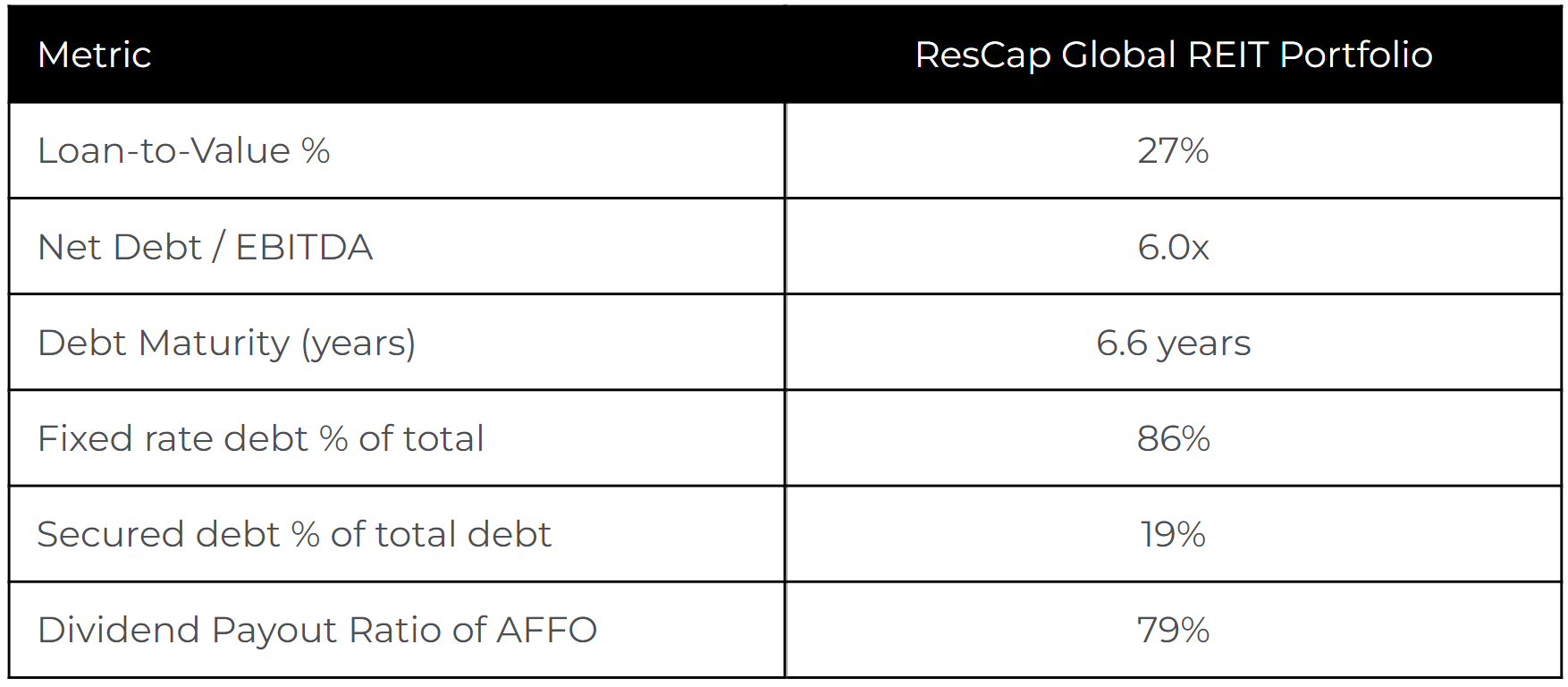

- Diversified sources of funding, with minimal reliance on bank debt (REITs in the RCL global portfolio source only 19% of their debt on a secured basis).

- A strong credit track record in the unsecured bond market, with most REITs rated investment grade8 and only two relatively small over-levered REITs ever having defaulted on unsecured public bonds.

- Relatively low forward property development commitments. Today we estimate the sector’s exposure to development is circa 5-10% of the industry’s total capital, versus 15% in 2007.

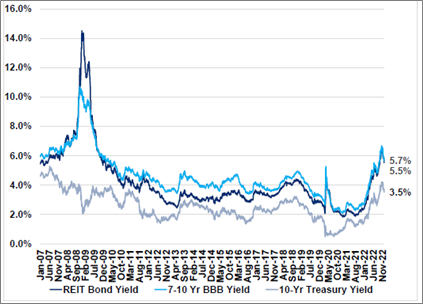

While 2022 saw the cost of debt increase for US REITs to levels not seen since 2009, US REITs have largely long-term fixed rate debt, therefore the increase in finance costs occurs gradually as existing facilities are refinanced.

REIT unsecured debt yields, BBB Corporate Yields and US Treasury Yields

Source: Citi Research, Factset

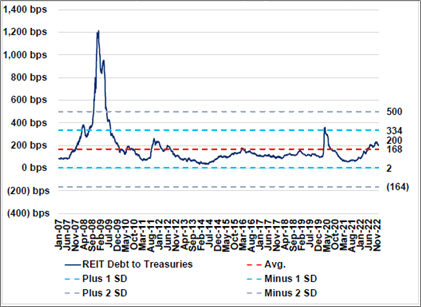

Importantly, much of the recent increase in interest costs has been due to rising base rates. Debt spreads are modestly above the long term (2007-22) average of 168 bps but have not spiked to levels seen in periods of acute distress such as the GFC (~1200bp) or the initial phase of Covid-19 (~340bp), suggesting that bond market investors are relatively comfortable at this point.

US REIT unsecured debt spreads to Treasuries

Source: Citi Research, Factset

Despite the banking turmoil, better quality REITs demonstrated they still have access to the unsecured debt capital markets at reasonable rates only weeks after the recent bank failures, with cumulative issuance of ~US$3 billion at spreads of 140-200bps.

One area of the credit markets showing signs of distress is the US office sector where spreads have spiked to circa 400 bps (similar to Covid-19 levels). Notably, debt spreads for one of the more highly levered New York office REITs, Vornado (VNO), have expanded to 550 bps.

Brief comments on Global REIT Ex-US debt

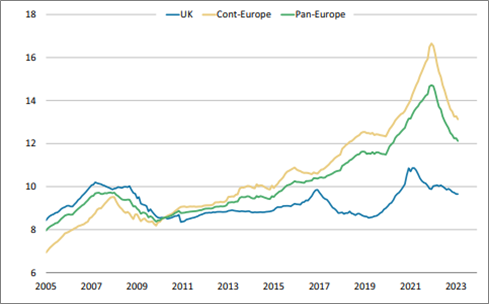

While this paper has focussed on the challenges in the US banking and office market, it is notable that Continental European real estate markets also face risks, albeit not necessarily relating to office operating dynamics. Continental European REITs stand out globally as more highly levered with many ignoring the lessons of the GFC and having increased leverage since.

Continental European REITs net debt/EBITDA remains elevated

Source: Morgan Stanley Research 03/2023

Of particular note, listed German residential landlords and many Swedish property companies are now capital constrained, and forced sellers of assets in a market with few buyers. Several have already cut dividends and we expect more will be forced to raise highly dilutive equity. The European market is more heavily reliant on bank finance than the US, although many of the larger European REITs have a diversified pool of debt capital providers. Despite the travails of Credit Suisse and suspicions about Deutsche Bank, European REITs thus far seem largely unimpacted by the banking stresses evident in the US.

For context, Continental Europe comprises just under 8% of the global REIT benchmark9. Consistent with our long-term investment philosophy, Resolution Capital remains sceptical of high leverage and thus remains underweight Continental Europe with less than 5% exposure. Our portfolio companies in the region exhibit lower leverage metrics than the European average.

Australian REIT balance sheets are relatively well positioned, with the lessons of the GFC still at the forefront of the minds of most management teams. Leverage is moderate at 27% debt/assets versus 40% in 2007. The larger REITs with investment grade credit ratings have access to the US unsecured corporate bond market, but smaller REITs are more reliant on bank finance and therefore tend to have shorter duration debt. Nevertheless, debt maturities are modest in the near term with less than 5% of debt expiring in 2023. Arguably the sector’s Achilles heel is that many AREITs had a higher proportion of floating rate debt, which put pressure on earnings in mid-2022 as interest rates increased rapidly.

Resolution Capital Global REIT positioning

The Resolution Capital global real estate portfolio is characterised by stronger balance sheet metrics than the broader universe of real estate owners. Therefore, in a more difficult credit environment, we believe most of our portfolio companies are relatively well positioned to withstand liquidity challenges, and potentially even capitalise on the distress of others. The table below highlights key balance sheet metrics for the Portfolio as at 31 March 2023 and the subsequent chart illustrates modest annual debt maturities for the Portfolio over the next three years.

Source: Resolution Capital

Rescap GREIT portfolio weighted average annual debt maturities

Source: Factset, Resolution Capital – weighted average

Conclusion

While small and regional US banks are important lenders to the commercial real estate sector, we believe the recent turmoil has limited direct implications for the listed REIT market. Over the past decade most REITs have improved their capital structures materially and diversified their borrowings away from banks to a range of capital providers. With few exceptions the REITs are positioned to be good customers for financiers which continue to be in the business of lending money to good quality credits.

There are important differences between the current banking crisis and the GFC, with commercial construction levels moderate relative to prior cycles. We believe the credit quality of the income producing commercial real estate sector is much better today than the sub-prime borrowers of the early-mid 2000’s, albeit the US office sector is vulnerable due to weak tenant demand.

Nevertheless, REITs do not operate in a vacuum, and it is important not to underestimate the risks of contagion if a rapid loss of depositor confidence, or the operational challenges facing the US office market negatively impact lenders appetite to finance the broader commercial real estate sector. We do expect higher credit losses in the real estate sector but we see limited evidence of excesses which threatens systemic failure. Clearly the US office market remains a risk to investors and lenders but at just 2.4% of the Global REIT benchmark, the risks appear to be contained.

Periods of distress often present investment opportunities. A period of moderate risk aversion can be a positive for well-capitalised landlords as it should lead to less funding for new property development, ultimately leading to less competitive supply over the next several years. In the meantime, the Resolution Capital Portfolio remains focused on REITs with strong balance sheets and resilient cash flows which are well positioned to withstand the near-term challenges and capitalise on future opportunities as they arise.

1 Mortgage Bankers Association data as at 22 March 2023

2 As at June 2021

3 Source: Federal Reserve 2022

4 Source: Bloomberg 2023

5 Source: Preqin Global Report 2023: Private Debt

6 Mortgage Bankers Association as at 22 March 2023

7 FTSE EPRA NAREIT index March 2023 – office sector excludes life science specialists Alexandria (ARE) and Biomed (BMR).

8 Per BofA; 66 of 88 US REITs rated by S&P are investment grade rated

9 FTSE EPRA NAREIT Global Developed Real Estate Index

Disclaimer: