Livewire: Why now is the time for your portfolio to gain exposure to nuclear power

Resolution Capital Global Listed Infrastructure (GLI) Portfolio Manager, Sarah Lau features in this Livewire article published on 18 February 2025, arguing that as the global electricity demand accelerates, so does the growth prospects of electric utilities in the global listed infrastructure sector.

20 countries have committed to tripping their nuclear capacity by 2025 and there are estimates this is an opportunity worth US$1.5 trillion.

But this isn’t the same nuclear that has been shrouded with safety issues and cost blow-outs in the past. And it’s certainly not the same nuclear you might have seen powering Springfield in The Simpsons!

Nuclear has changed

Generation 3 reactors have advanced nuclear power generation into a new era of safety and efficiency. These are reactors with enormous containment improvements, they use natural process such as gravity for safety and have simpler designs. The bottom line is, they are built in a way that means they cannot melt down.

Below you can see a timeline of nuclear power plant commissioning in the United States.

You can see that most were constructed in the 1970’s and 1980’s. During that period there are 50 different designs across the fleet of around 100 nuclear power plants.

![]()

The reactors of the 70’s and 80’s were like snowflakes. The technology never scaled.

But cast you eye over to the right side of the chart.

Those two units that came into service in 2023 and 2024 were built by a company called Southern Company. They are known as the Plant Vogtle Units 3 & 4.

The initial cost estimate to build the two units was US$15 billion. The construction process was interrupted by COVID, while Westinghouse (the reactor manufacturer) went bankrupt.

The cost ended up being US$32 billion and construction took 10 years, which was roughly double the initial estimate.

However, the U.S. Department of Energy notes that this was a first-of-a-kind project for a Generation 3 reactor.

Today, the advanced Vogtle 3 & 4 units are powering about one and a half million households. The industry can now take a ‘cookie-cutter’ approach to manufacturing the units which we think will lead to efficiencies and therefore lower cost and quicker build times.

Demand for nuclear

Electricity demand is a critical issue in economies across the world that needs to be solved.

We’ve illustrated annual electricity load growth in the United States in the chart below.

![]()

For the past two decades, there’s barely been any electricity demand growth. That’s because population growth and new applications have been offset by energy efficiency innovation (think LED lights and appliances with power saving functions).

But as we move into the 2020s, we’ve seen AI, data centres, and advanced manufacturing begin to consume more power than ever before.

Every single query on ChatGPT takes 10 times the amount of power that Google Search takes, and it’s important to remember, we’re still in the very early stages of AI with the technology likely to broaden out well beyond the current applications and big players.

For investors, being conscious of this increasing demand for electricity is important.

Infrastructure is the real asset class for structural growth

On top of the existing infrastructure investment super cycle that has been underpinned by the global energy transition and decarbonisation investment, the current acceleration in electricity demand ads additional layers on top of this cycle.

We believe building exposure to electric utilities in the global listed infrastructure sector is a sensible way to play this super cycle, and it’s nuclear utilities in particular, that we think provide very attractive growth prospects in 2025 and well beyond, because nuclear is perfectly suited to power AI.

If you consider that most tech companies (including the hyperscalers) have decarbonisation goals that they haven’t stepped away from, nuclear provides a sound solution.

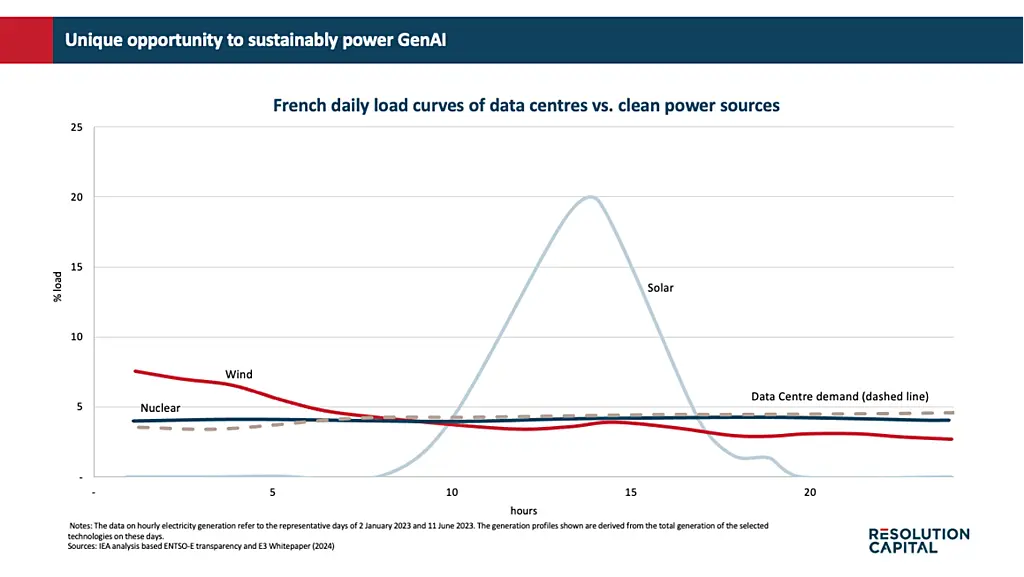

While solar has a very specific and defined peak during the middle of the day when the sun is out, and wind has significant variability, the consistency of nuclear power matches the demand profile of a data centres almost perfectly.

65% of existing nuclear power plants are owned by listed US utilities. These include the following two high conviction portfolio holdings in the Resolution Capital Global Listed Infrastructure Fund.

Southern Company (NYSE: SO)

This is a monopoly electric utility with assets in Georgia, Alabama, and Mississippi.

As mentioned earlier, Southern Company went through a difficult period when building Vogtle Units 3 & 4. It was write-down after write-down. Along with the rest of the market, we thought that after the construction of Vogtle, Southern will go back to being a boring electric utility that provides predictable returns.

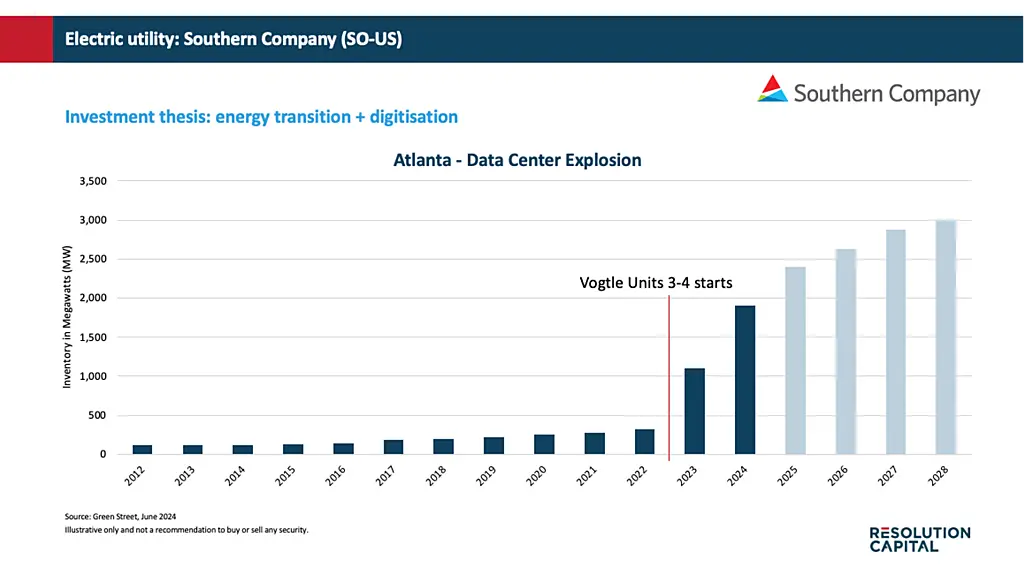

Our property team keeps a close eye on the data centre market and what we gathered from them can be summarised in the chart below – the data centre demand and the forecast of supply of inventory of data centres in Atlanta is exploding.

As the monopoly utility, Southern is allowed to earn a reasonable rate of return for such investments, which we think will lead to higher earnings for a longer period than the market is realising.

Constellation Energy (NASDAQ: CEG)

Constellation owns a quarter of the nuclear fleet in the U.S.

When this stock was initially spun out, it didn’t meet Resolution Capital’s investment criteria as it was exposed to commodity power prices.

But then the U.S. Government realised the strategic value of 24/7 emissions-free power was worthy of underwriting. This means that today, the cash flows of this company are defensive, and inflation linked.

Constellation Energy can now contract at prices above that U.S. Government guarantee and above market prices.

One of the units at Constellation’s Three Mile Island site (pictured below) was shut in 2020 when power prices were very low and before the aforementioned U.S. Government underwriting came in.

Last September, it was restarted after Microsoft entered a 20-year contract with Constellation to purchase power off them. We calculate roughly a 25% internal rate of return for the duration of the 20-year Microsoft contract.

Image: Constellation Energy

The company also has strong balance sheet and cash flows that can assist in realising the optionality of their sites and provides strength to undertake buybacks and bolt-on acquisitions.

We started buying the stock in the Resolution Capital Global Listed Infrastructure Fund at $80. It’s currently trading at over $300.

Invest in a portfolio of global listed infrastructure assets with Resolution Capital

Across all of Resolution Capital’s listed real assets strategies, we seek to invest in high quality assets, capable management teams with skin in the game, and sensible capital allocation.

The nuclear renaissance and the portfolio holdings outlined above are just a snapshot of some of the structural growth opportunities – including in the energy transition, energy security, and mobility – that we provide exposure to through the Resolution Capital Global Listed Infrastructure Fund.

The Fund is deliberately designed for clients looking for exposure to a defensive growth asset class that’s ideal for compounding wealth.

The Resolution Capital Global Listed Infrastructure Fund is available to investors via an unlisted trust, and will soon be quoted on the ASX as an active ETF under the ticker ‘RGIF’ (pending final regulatory approvals).

Further information

Contact Resolution Capital Client Services team at clientservices@rescap.com

Disclaimer:

This communication is prepared by Resolution Capital Limited (‘Resolution Capital’) (ABN 50 108 584 167, AFSL 274491). Pinnacle Investment Management Limited (ABN 66 109 659 109, AFSL 322140) and its associated entities (collectively ‘Pinnacle’) provide distribution and responsible entity services to Resolution Capital.

Resolution Capital and Pinnacle believes the information contained in this communication is reliable, however, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. This communication is general information only and does not take into account your objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so and consider the appropriateness of the information having regard to your specific circumstances. To the extent permitted by law, Resolution Capital and Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Resolution Capital.

Resolution Capital is an affiliate of Pinnacle Investment Management Ltd. Pinnacle Investment Management (UK) Ltd is an appointed representative of Mirabella Advisers LLP (FRN 606792), which is authorised and regulated in the UK by the Financial Conduct Authority.