Australian Residential – Build To Rent Takes Center Stage

By almost any measure, residential property is the largest real estate sector in Australia. Whilst listed property companies such as Stockland and Mirvac are actively involved in residential property development and trading activities, termed “Build to Sell” (BTS), there is limited exposure on the Australian Stock Exchange to REITs which specialise in long term residential property ownership1.

Indeed, more broadly, unlike the case in some international markets, Australia’s private housing rental sector has remained largely “un-institutionalised” with most residential rental dwellings, detached houses and strata title unit blocks, owned separately by a broad range of typically smaller, “mum & dad” investors.

Relatively new to Australia, Build-to-Rent (BTR) residential property is now experiencing a wave of interest from developers and institutional investors. BTR involves developing residential buildings for the sole purpose of rental. Typically multi-storey and divided into multiple self-contained units2, the entire building is usually owned and managed by a single entity. Commonplace in the U.S., these properties are termed “multi-family residential” or apartments as distinct from individually owned residential strata units which are termed “condominiums”.

Recently, Australian REITs such as Mirvac (MGR) and Stockland (SGP) have launched BTR initiatives and outlined plans to significantly increase their exposure to this emerging sector, whilst developer Lendlease (LLC) and offshore private equity groups such as Starwood and Greystar have also been leading the development charge. Furthermore, local listed retail landlords such as Vicinity Centres (VCX), as well as New Zealand’s Kiwi Property Trust, are also including BTR as part of mixed-use development of their shopping centres.

The overseas experience

Institutional ownership of dedicated apartment rental buildings is common in Japan, Continental Europe and North America. It is also becoming more popular in the UK.

In these markets ownership of dedicated rental multi-family buildings is a long-established staple real estate investment for institutions and high net worth individuals.

Dedicated listed residential investment companies are a major component of the global REIT universe, a number of which are highlighted in the table below.

Source: Company filings, Factset, Resolution Capital (July 2023)

The properties are located in urban and suburban settings consisting of mid/high rise towers and garden style apartment communities. In order to achieve operating efficiencies, multi-family properties typically comprise between 50 to 500 dwellings, but larger communities are not uncommon. In terms of apartment size, they range from studios up to generally 3 bedrooms, however most are 1 and 2 bedrooms. In the U.S., the typical tenant age is 25-40 years old with an average of 2 residents per home.

Generally, the apartments are leased on a 1-year contract but longer terms can be negotiated. The resident is afforded a right to renew, depending on the jurisdiction, at a regulated or market rental rate.

In virtually all markets new tenants pay the prevailing market rent. However, in some markets sitting tenants are afforded some protection from rent increases during their occupation. In many parts of Europe and Canada, rent increases for renewing tenants are regulated by the government, typically capped at or below inflation and sometimes averaged over a number of years to smooth out any short term market rent spikes. In the U.S., UK and Japan, rents for new and renewing leases are generally subject to market driven changes. That said, some U.S. cities including New York apply rent increase caps, if a property was granted land tax benefits as part of the original development process. Meanwhile some areas of California impose a limit above inflation, a system similar to the situation in Canberra.

It is expected that most states of Australia will operate in a regulation light environment. However, we note the Victorian government is considering introducing a range of new regulations including no rent reviews for 2 years and caps on rent increases. We expect this poses a major challenge for the industry and will act as a deterrent to investment.

From a renter’s perspective there are several advantages of BTR housing including:

- Peace of mind that they will not be evicted at the end of the lease which can be the case when condominium owners have other plans for the property such as owner occupation or selling the property;

- Professional property management often with on-site/24-hour maintenance teams and provision of additional amenities and services aimed at convenience. These services include smart home technology packages incorporating connected wifi and remote climate control; and

- The absence of friction with owner occupiers sharing condominium buildings.

Depending on the market, target renter and the extent of competition, the apartment complex may come with a range of amenities, fixtures and fittings. Apartment communities in the U.S. tend to be amenity rich, providing tenants with access to on-site facilities such a pool, gymnasium, sauna, bbq, media rooms and libraries. Whilst typically unfurnished, the apartments will include complete fit-outs of kitchens (including fridge) and laundry (including washing machine/dryer). Pets are generally permitted in U.S. apartments, however there are some restrictions on size and breed, and tenants pay an additional monthly pet fee.

Equity Residential kitchen. Accessories are for display purposes only

Source: Company website

The BTR sector is relatively new to the UK, and it is not uncommon for the apartments in this market to include a basic furniture package.

At the other end of the spectrum, apartment buildings in many German cities have minimal amenities and the units are offered on a ‘cold shell’ basis, that is, leased without kitchen fit-out (cabinetry, sinks and appliances), light fixtures and floor coverings. For this reason, along with high tenant protections in the form of regulations governing rent increases for sitting tenants, the average stay for a German resident is over 10 years, versus less than 2 years in the U.S. Most German apartments are 2 bedrooms of circa 65 sq m. It should be noted that many apartments owned by the listed German residential companies are aimed at the “affordable” segment, built in the quarter century following 1945, often as worker accommodation and originally owned by corporates or local housing authorities3.

German rental, bedroom left photo, kitchen right

Source: rentola.com

Given the talk about the lack of rental affordability we would have expected local product would be at a basic level. However, from what we have observed, newly developed Australian apartment buildings have extensive amenities. The properties we have inspected come with shared gym, pool, sauna, outdoor and indoor cooking facilities, office/work spaces and in some cases a podcast production room.

Given the extent of the amenities, it should be no surprise that rental pricing of the apartments is pitched at mid to higher income brackets which we believe enables developers to command premium rents in order to achieve enhanced returns. We have heard of the rent to household income ratio for a recent BTR development in Melbourne being as high as 35%, much higher than the average in the U.S. of 20-25%. Unusually, and for reasons we cannot fully fathom, Mirvac has decided to forgo tenant rental bonds (security deposits).

Why has Australia been slow to develop Residential for Rent?

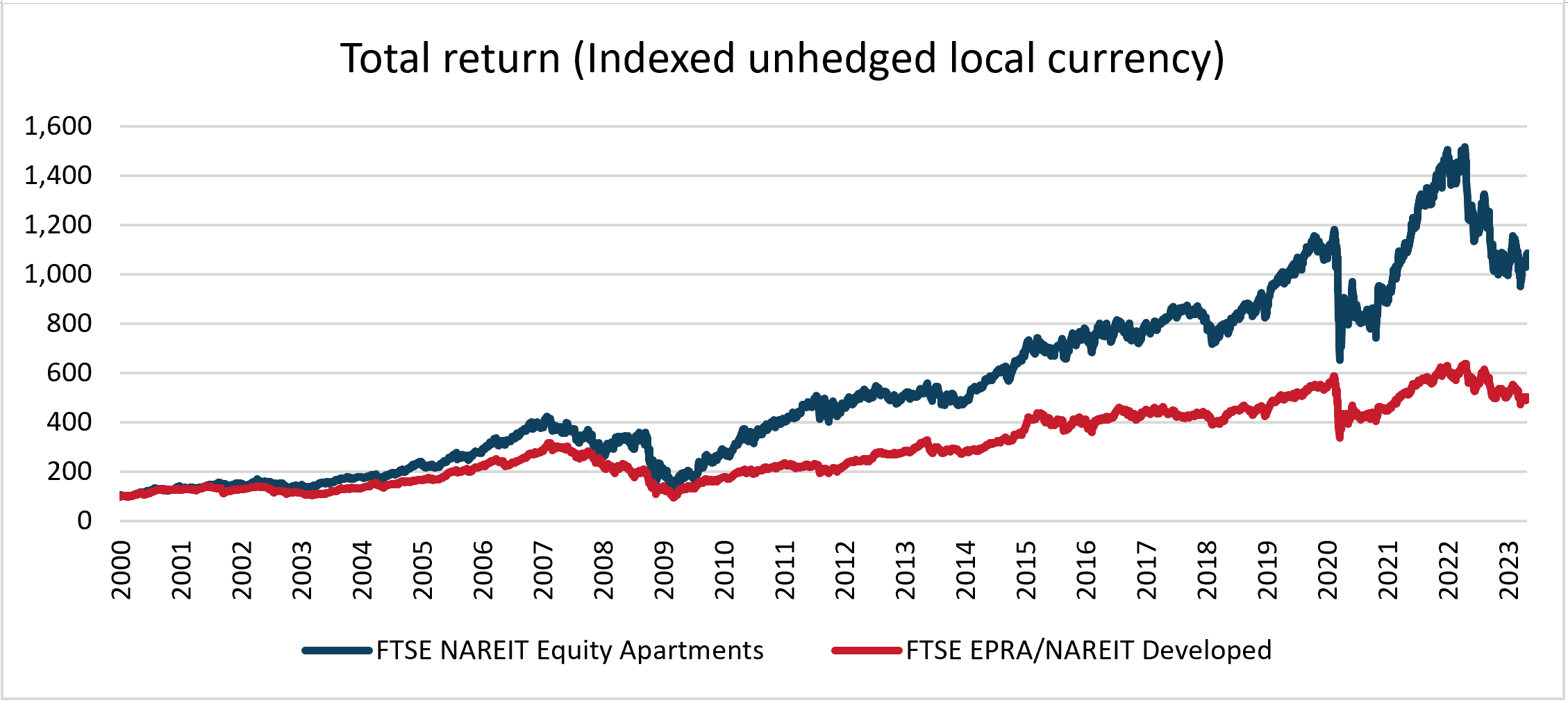

It is evident that the international apartment REITs have generated superior long term returns to the overall listed real estate sector as highlighted in the chart below.

Source: Factset, Resolution Capital (July 2023)

Which begs the question of why the sector has not been a feature of the Australian commercial property investment landscape?

It is likely that several factors have contributed to the limited development of dedicated multi-family housing to date in Australia. It is fair to say that institutional investors have under appreciated the superior returns for residential. Historically, a key hurdle has been the initial income yield spread between residential and non-residential commercial investment property has been too wide: Australian residential apartment net rental yields have typically been below 4%, typically below the interest cost of debt finance, whereas office, retail and industrial property yields have traded on yields more than 6%. This is not the case in the U.S. where residential property yields are not dramatically different to commercial property. Furthermore, periodically, governments have provided incentives such as land tax abatements to encourage residential development.

By contrast, longstanding Australian state government policies have encouraged home ownership through first home buyer grants whilst federal taxation measures such as negative gearing and capital gains tax (CGT) concessions have favored individual ownership of private rental properties. Separately, Australia’s high withholding tax for foreign investors has put offshore institutional capital at a distinct cost disadvantage to that of local investors. Meanwhile, developers have been motivated by the superior immediate development profits offered by build-to-sell (BTS) projects amidst general buoyant housing market conditions, that is, sold as condominiums to a mix of owner occupiers and investors.

What’s changed?

Recent local and international institutional interest in the sector has been fueled by cap rate compression between commercial and residential yields, robust residential rental fundamentals and changing government policy attitudes toward housing supply to address affordability issues and provide greater choice for the end user.

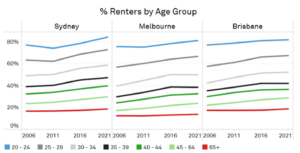

The housing affordability challenge is facing ongoing pressure from insufficient new housing supply and increasing demand from an expanding renter population (highlighted in the charts below) accentuated by higher levels of immigration, and longer-term declining household size.

Source: ABS, Charter Keck Cramer (July 2023)

As a result, home ownership affordability is poor, residential vacancy rates are at record lows and rents are surging.

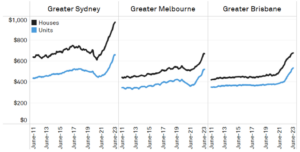

Australian East Coast Residential Rents

Source: SQM, Charter Keck Cramer

Given the underlying conditions, governments and investors are focusing on BTR as a solution to provide more housing options. Hence, both state and federal governments have taken steps to level the playing field to encourage capital from different savings pools in order to create more and varied supply.

A reduction in the Federal Government’s Managed Investment Trust (MIT) withholding tax rate for foreign investors on BTR assets has been a catalyst in attracting offshore investors to the sector, with the change estimated to have a positive 100-250 basis point impact on returns over a ten-year period. Furthermore, state governments are taking proactive steps by offering planning and development incentives for projects that incorporate affordable housing components, including fast tracking the approval process.

Part of these government initiatives can be attributed to recognition of changing demographics and lifestyle changes. We should also recognise that not everyone can or wants to own a property (e.g., job mobility, transition phases of life, aversion to debt) and therefore there are arguments in favour of professionally managed dedicated rental living.

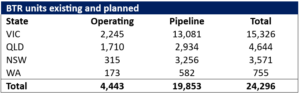

It is important to recognise this is not likely to change the housing dynamics materially in the short to medium term. As the table below highlights, the total number of units built or currently under development in Australia totals less than 25,000. Assuming a 2-year development timeframe, the pipeline represents roughly 5% of total annual new housing construction. In many cases, BTR projects are being developed on sites which would have otherwise been developed for sale as BTS strata-titled apartments of perhaps a similar scale, thus not adding to total supply but at least adding to the rental inventory.

Source: Macroplan (July 2023)

At this point, the growth of BTR should be viewed as attracting a broader pool of capital to hopefully encourage more supply and provide people with more choice and a superior product. If BTR is to contribute meaningfully to increased supply, Governments will need to help reduce building costs and provide more incentives, most likely in the form of concessions for greater building density.

Hence, it is likely that developing affordable rental units nationwide in attractive key locations will continue to be a considerable challenge for the Australian BTR sector. Australia’s current estimated development yields of 4.5% are much lower than the U.S. where established players are able to generate stabilised yields of ~6%. We attribute the lower yields to substantially higher land and building costs, partly the outcome of higher residential valuations for residential in Australia in general.

Therefore, as we highlighted earlier, to overcome high land costs and increasing construction costs, many BTR developments in Australia have been designed and marketed as premium apartment communities, with an emphasis on tenant lifestyle and community experience.

Thus, BTR in its current form falls short of offering a scalable and affordable solution to help ease Australia’s housing troubles. Striking a balance between affordability and investor return will be key to the evolution of the sector over the long term. Hence, we see this as a promising sector but is, in its current form, unlikely to materially change the residential landscape in the short to medium term.

1 Aspen Property Group, an emerging but still small ASX listed REIT, has focused on affordable rental housing, whilst Ingenia Communities provides a range of residential accommodation.

2 There are U.S. residential REITs also focused on free-standing-single-family home rental (SFR) properties. Currently in Australia there are no private platforms focused on buy or develop-to-own SFR. This sector requires significant critical mass to defray management costs and is largely isolated to the U.S. where large portfolios were created out of mass mortgage foreclosures during the 2008-2010 Great Financial Crisis.

3 The rent regulated market conditions have served to maintain a significant stock of now ageing affordable housing but have acted as a hurdle to the development of meaningful quantities of contemporary housing as rents and capital values are often significantly below replacement cost.

Disclaimer: